1. Background

Decentralised finance (DeFi) aims at democratising finance by replacing centralized financial institutions with direct, peer-to-peer relationships for improving the availability and efficiency of the financial services. DeFi mainly uses blockchain technology, cryptocurrencies and smart contracts to manage wide variants of financial transactions.[1]

The below figure enlists certain financial transactions and how they are managed in DeFi vis-a-vis traditional finance:

Source: Alexandra Born et al., Decentralised finance – a new unregulated non-bank system? (https://www.ecb.europa.eu/pub/financial-stability/macroprudential-bulletin/focus/2022/html/ecb.mpbu202207_focus1.en.html)

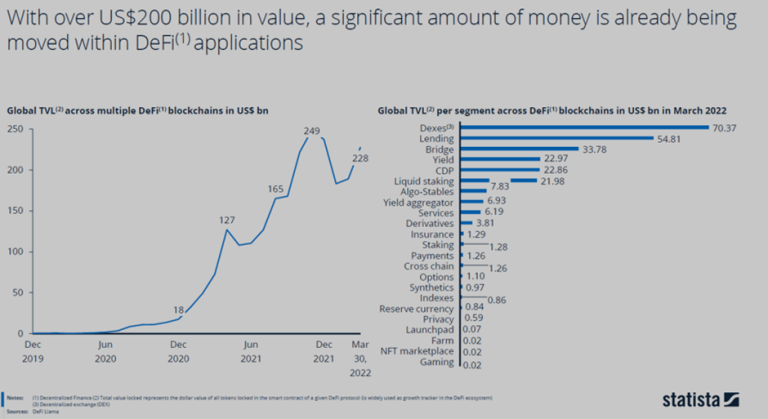

The below image shows some statistics around total value locked in DeFi as of March 2022.

Source: Digital Economy Compass 2022 – Chapter 1, The ascent of the crypto economy (Statista)

The purpose of this blog is to discuss tax implications on certain DeFi transactions. (covered in next section)

2. Tax implications based on the different variants of the transaction[2]

Several countries around the world have already laid down certain guidelines for taxation of DeFi transactions. Some are in the process of laying down the guidelines. For example: UK released public consultation in relation to the taxation of DeFi transactions for lending and skating of the cryptoassets.

Certain DeFi transactions are discussed below (this is not an exhaustive list of transactions):

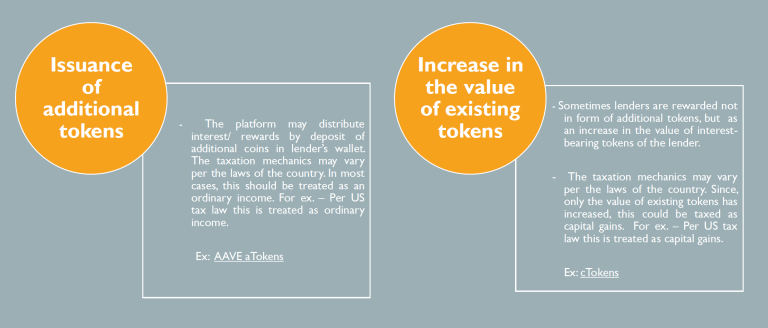

a. Lending transactions:

b. Staking and interest income

c. Governance token

d. Others

3. Conclusion

The determination of tax implications in case of DeFi transactions should be based on facts, circumstances and actual nature of the transactions. The taxation mechanics for the same DeFi transaction could vary across countries based on the local tax laws of the countries.

In all:

- Exchange of one token with another in most cases would be taxable (where applicable) under the head capital gains.

- Crypto currency earned directly in most cases would be taxable (where applicable) as ordinary income.

[1] https://pelaghiaslaw.com/2022/03/24/decentralized-finance-defi-the-european-regulatory-perspective/

[2] https://tokentax.co/blog/defi-tax-guide; https://cryptotaxcalculator.io/blog/the-ultimate-defi-tax-guide/

For slides refer below :

Related Posts

July 30, 2023

Non-Fungible tokens – Case study (Transfer pricing implications)

Click here to view the slides.

July 30, 2023

Metaverse and trademark rights

1. Background and ongoing developments Trademarks help to identify the goods and services and distinguish them…

July 30, 2023

NFTs and copyright issues

NFTs or ‘Non-Fungible Tokens’ are digital files having a unique identity that is verified on…